Click to invest now

Introduction

When the Covid-19 pandemic swept through the world, much about our daily lives changed forever. One of the biggest shifts was the embrace of remote work. Today, approximately 35% of U.S. workers work from home some of the time and 26% are fully remote. In fact, 16% of U.S. firms are now fully remote, with no formal office presence at all. To put this in perspective, prior to the pandemic only 5.6% of workers worked remotely.

This shift has caused sweeping changes to the commercial real estate world with many office buildings experiencing leasing issues and some buildings sitting fully vacant. The idea quickly emerged to convert unused office space into multifamily housing. Unfortunately, this is a great idea in theory but tougher in execution.

The number of vacant office buildings being converted into multifamily housing has been rapidly increasing. In just three years, office-to-residential conversions have nearly tripled and now account for 42% of all adaptive reuse projects, according to RentCafe. Major cities, including New York, Washington, D.C., and Los Angeles, are encouraging these conversions through incentives, and developers are actively purchasing distressed office properties. With a vast potential of 1.2 billion square feet of office space suitable for conversion, this trend shows no signs of slowing down.

But here’s the reality: while these projects generate plenty of headlines, the actual execution rate is far lower than many would expect. High construction costs, strict zoning laws, and painfully slow approval processes have kept many of these ambitious plans stuck in neutral. For investors looking at the multifamily space, the key question isn’t just how many conversions are being announced—it’s how many will actually get built and deliver value.

On the surface, the logic for conversions is simple. Office demand has permanently shifted due to remote and hybrid work, leaving many older buildings underutilized. Meanwhile, the U.S. has a housing shortage, particularly in the workforce and affordable housing segments. Combine those two trends, and conversions should be a no-brainer.

And to an extent, they are—when the numbers work.

The best candidates for conversion are typically older, functionally obsolete office buildings with smaller floor plates and large window lines, making them easier to reconfigure into apartments. These buildings often sit in prime urban locations where demand for housing is high, and some local governments are beginning to incentivize adaptive reuse by cutting red tape or offering tax breaks.

Developers who can execute these conversions efficiently stand to benefit from:

But for every project that pencils out, there are many that don’t.

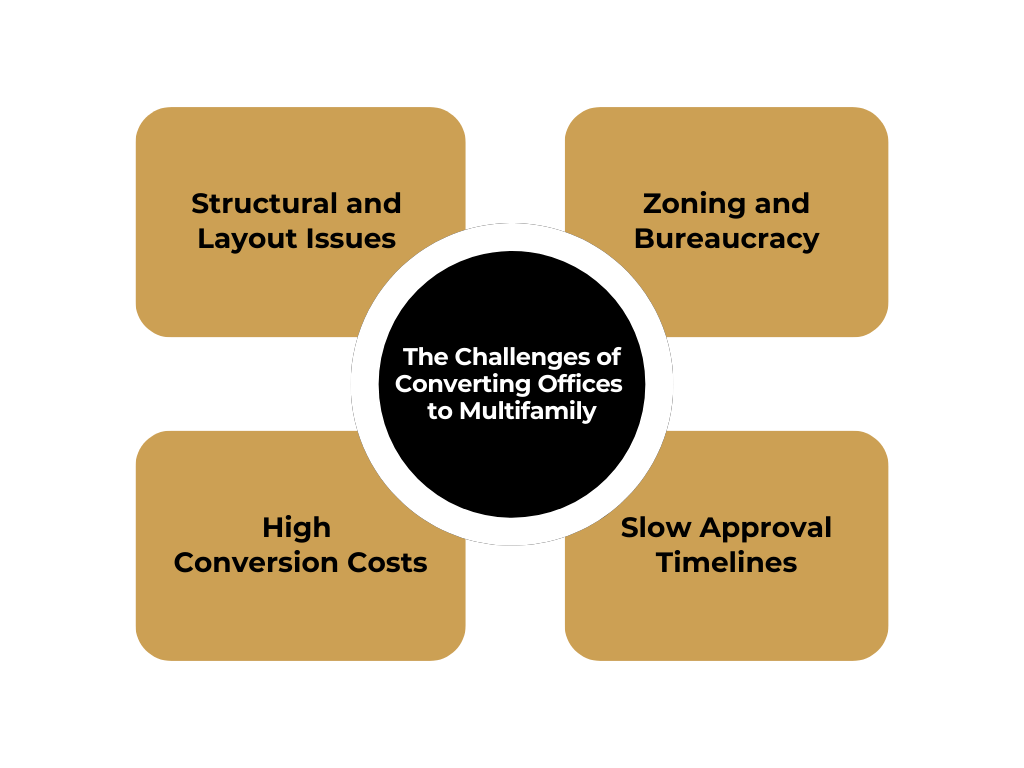

Despite the hype, the reality is that converting an office to an apartment building is far from a simple swap. The hurdles can be significant:

> Structural and Layout Issues – Office buildings weren’t designed for residential use. Large floor plates make it difficult to create units with adequate natural light. Plumbing, HVAC, and mechanical systems often need to be completely overhauled, which drives up costs.

> Zoning and Bureaucracy – Many cities still classify these buildings strictly for commercial use, meaning developers have to navigate rezoning, variance approvals, and public hearings—processes that can take years.

> High Conversion Costs – Even with cheaper acquisition costs, the price tag for converting an office into apartments is substantial. A building might be “cheap” to buy but require millions in gut renovations before it’s even rentable. In some cases, it’s actually more expensive to convert an office building than to build new from the ground up.

> Slow Approval Timelines – Even when cities claim they want to support conversions, the approval process remains painfully slow. In places like New York and San Francisco, where development is already a bureaucratic nightmare, these delays kill many projects before they ever break ground.

So, where does this leave real estate investors looking at the multifamily space?

First, while conversions are a great talking point, they aren’t a silver bullet for the housing shortage. Yes, some projects will get done, but the sheer volume of vacant office space won’t magically turn into housing overnight. That means traditional value-add multifamily investments will continue to be the strongest play for consistent, scalable returns.

Second, investors should view office-to-multifamily conversions as an interesting niche opportunity, not the future of the entire market. Some developers will navigate the hurdles successfully and create fantastic projects, but for the average investor looking for strong, reliable returns, existing multifamily assets with proven cash flow remain the better bet.

Office-to-multifamily conversions make sense in theory, but in reality, they’re incredibly difficult to execute at scale. While cities are pushing to make these projects happen, the actual number of units that will be delivered remains a fraction of the pipeline.

For investors looking to build wealth in multifamily real estate, the best opportunities remain in well-located, cash-flowing apartment communities with strong demand drivers. The housing shortage isn’t going anywhere, and well-run multifamily assets will continue to outperform.

That’s why, at Faris Capital Partners, we focus on value-add apartment investments in high-growth markets where we can execute proven strategies to increase cash flow and long-term appreciation. If you’re interested in learning more about how we help investors build wealth through multifamily, let’s talk.

👉 Schedule a call with our team today to discuss your 2025 investment strategy.